International climate policy under the war on Ukraine

© Plainpicture / Elektrons 08

The invasion of Ukraine by the Russian Federation has huge impacts not only on Ukraine, but also on the global political order and on economic relationships. In this blog, we discuss some of the impacts which are related to climate policies. These include impacts on energy prices and energy security, the importance of resilience and diversification of energy supply, and impacts on the transformation of energy systems and on the international climate negotiation process. This blog is an excerpt of chapter 6 of the study ‘The COP27 Climate Change Conference – Status of climate negotiations and issues at stake’.

Impacts on energy prices and energy security

The Russian Federation is a key supplier of fossil fuels to international markets: around 20 percent of natural gas and coal, and around 10 percent of crude oil in global export volumes came from Russia in 2020. The EU is particularly dependent on fossil fuel supply from the Russian Federation. In 2021, the EU imported more than 40 percent of its total gas consumption, 27 percent of oil imports and 46 percent of coal imports from Russia. In the months before the invasion, natural gas supply volumes to Central Europe were reduced compared to previous years, and natural gas storages were not filled to the same levels as in previous years, which has spurred increases in natural gas and electricity prices since the autumn 2021. After lockdowns due to the COVID-19 pandemic in 2020, the economic recovery in 2021 led to a strong increase in coal demand, in particular by large importers such as India and China, which induced coal prices to increase in 2021.

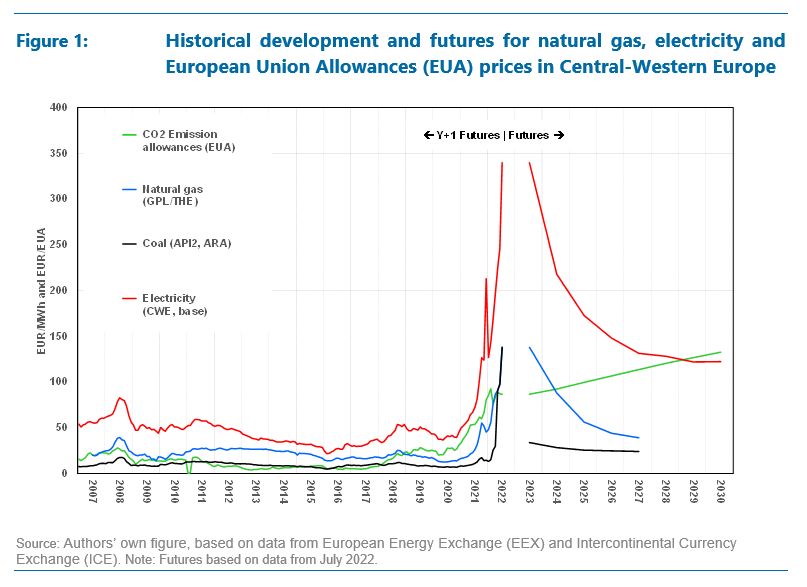

Prices for natural gas have multiplied

After the Russian Federation’s invasion in February 2022, these market trends escalated and decreased natural gas supplies brought about prices increases for natural gas. The figure below shows the wholesale price development for natural gas deliveries in Central Western Europe, coal delivered to Western European ports, electricity in the Central European electricity market and CO2 allowances from the EU ETS. Mainly as a consequence of reduced gas supply from the Russian Federation, prices for natural gas have multiplied. In the last 10 years, natural gas traded slightly above 20 EUR per MWh HHV (Euro per mega-watt hour – higher heating value) and prices stayed at that level until beginning of 2021. Since then, they have reached price levels of 200 EUR/MWh in summer 2022 (Average TTF-spot price in July and August 2022).

Coal-fired power generation has increased

In order to compensate for reduced natural gas-fired electricity generation, coal-fired generation has increased – along with a continued increase in coal demand in India and the prospect of an embargo on coal from the Russian Federation (see paragraph on sanctions further below) – driving coal prices even further. Between mid-2021 and mid-2022, coal price in Europe have more than 10-fold. With strong increases in cost for the main price-setting generation technology in the electricity market, electricity prices in the EU have also increased considerably. Forward contracts show decreasing natural gas, coal and power prices in the years ahead. However, the era of low fossil fuel prices seems to be over, with all prices staying clearly above the level observed before the war.

The price of CO2 allowances reaches new heights

The nominal price for CO2 allowances stayed below 30 EUR/tCO2eq until end of 2020. Since then, it has increased to levels above 90 EUR/tCO2eq in winter 2021/2022. Futures indicate a further moderate increase to levels of around 100 EUR/tCO2eq in 2025 and 130 EUR/tCO2eq for 2030. Along with the European Union’s Fit-for-55 Package, the increase of the natural gas price is an important driver for the allowance price. A fuel switch from natural gas to more carbon-intensive fossil fuels (such as fuel oil in heating and coal in power generation) leads to an increase in demand for allowances in installations covered by the EU ETS and hence to higher prices.

Sanctions in the wake of the Russian Federation’s war on Ukraine

As part of the sanctions imposed as a reaction to the Russian Federation’s war on Ukraine, several countries imposed bans on fossil fuel imports from Russia. The U.S. and Canada banned all fossil fuel imports from Russia. By end of 2022, crude oil and oil products from Russia will also be banned in the UK. After difficult negotiations, the EU has also agreed on bans for coal, crude oil and numerous oil products. Starting in August 2022, coal and other solid products cannot be imported from Russia to the EU. A ban on crude oil will come in effect by December 2022. While there is an exemption for pipeline-bound imports, Germany and Poland include the import of pipeline-bound oil in their sanctions portfolio. These restrictions will cover nearly 90 percent of Russian oil imports to Europe by the end of the year 2022. While preparing these sanctions, EU countries had already been working on reducing imports.

The sanctions imposed by the EU and other countries are to some extent made up by increased imports of other countries, making use of spare volumes. With buying 18 percent of Russia’s exports in May 2022, India became a significant importer. It is important to note that significant shares are re-exported again as refined products to destinations also including Europe and the US. Similarly, Saudi Arabia has increased its crude oil imports from Russia after the invasion. They are used to a domestic oil-fired electricity supply, while domestic production is freed up for exports. This seaborne trade relies on tanker capacities. Potential future physical shortage of tanker capacity or the agreed extensions of sanctions to insuring ships carrying Russian oil could significantly diminish Russian capacity to export oil. China is another beneficiary of reduced deliveries to the EU. However, east-bound export capacities for fossil fuel are limited and already running at high-capacity utilisation rates. Therefore, another substantial increase in imports would require either very long and costly shipments from Russia’s Baltic Sea and Black Sea, or new infrastructure that would take years to build.

The resilience of the energy system becomes a key factor

The EU is addressing the issue of security of supply in terms of fossil fuel supply by reducing consumption, increasing capacities of alternative sourcing routes from international markets and activating new trade partners. With the uncertain future of Russian natural gas supply, the concepts of resilience of the energy system and diversification of energy supply are nevertheless becoming key factors in energy planning. It is important to increase the resilience and the diversification of pipeline-bound energy supply (natural gas and oil). This challenge is particularly large for natural gas. Resilience always has a supply side and a demand side. On the supply side, several Member States in the EU have increased or are increasing their liquefied natural gas (LNG) import capacity (Finland, Netherlands, Germany), e.g. by chartering floating LNG storage and regasification unit (FSRU) terminals.

Measures for demand reductions

On the demand side, a wide variety of measures are being taken. These range from increased use of coal and oil power plants that replace production from natural gas power plants in the power sector, a fuel switch from natural gas to fuel oil or LPG (liquefied petroleum gas) within one installation, or reducing demand for fossil fuels. Demand reductions can be achieved by reduced heating or a change in supply chain (sourcing of final products instead of production in the EU of, for example, ammonia).

In the long term, the roll out of renewable energies in the EU as pursued by the policies under the EU’s 2030 climate and energy framework and the REPowerEU Plan is the most important measure for increasing the resilience of the European energy supply.

The challenge about increasing the resilience and diversification of the energy supply is that a lock-in into a carbon-intensive infrastructure should be avoided:

-

Extending the life of old coal fired power plants for a few years does not constitute a lock-in, but scrapping coal phase-out plans altogether would be problematic.

-

Chartering flexible FSRU terminals for a decade in order to be able to import more LNG does not constitute a lock-in, but the signature of very long LNG-supply contracts or investments into new fossil gas fields does.

While there might be a new incentive to invest into additional fossil fuel production infrastructure, it will not be compatible with a 1.5° world.

Impacts on the transformation of energy systems/decarbonisation in Europe

Many countries in Europe and world-wide planned on using natural gas as a bridging technology until fossil fuels can be replaced completely by renewables. Such plans need to be revisited now that the supply of gas from the Russian Federation may cease as a consequence of political conflict or sanctions.

In the past fossil gas was considered a bridging technology, providing flexible generation in the power sector until the roll out of renewable energies have been achieved. For the future this role will be discussed. To increase the security of supply, it is not necessary to completely abandon the use of natural gas. In some cases, it is sufficient that natural gas can be substituted when necessary. Bivalent plants that can use different fuels will become more important (fuel oil and LPG can replace fossil gas).

The role of natural gas

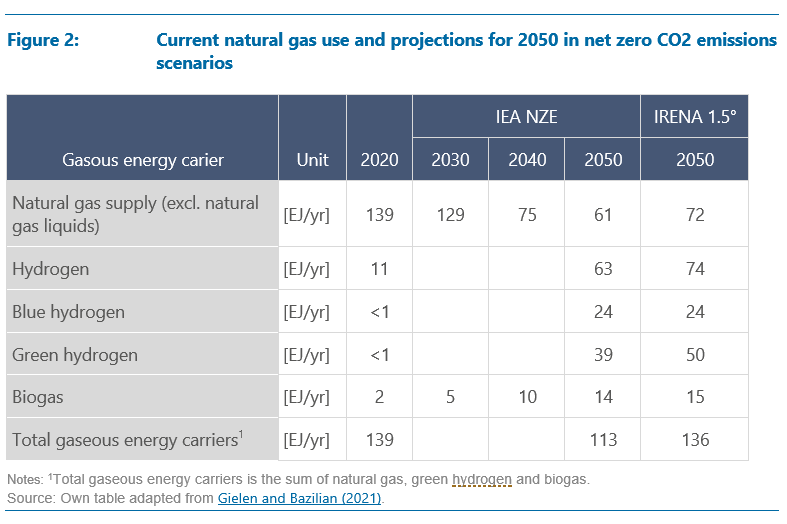

While natural gas still plays a key role in net zero scenarios, its central contribution is mainly in the horizon until 2030. As shown in Table 5 natural gas supply was projected to decrease by only 10 EJ (Exajoule) between 2020 and 2030. Given the fact that many countries have been planning on substituting coal-fired power generation by increasing natural gas-fired generation and ramping up natural gas-based blue hydrogen production, the increase is overcompensated by a decrease in demand from other sectors like from energy efficiency in the building sector. After 2030, total demand is projected to decrease substantially, arriving at about half (61-72 EJ) in 2050. At the same time the share of natural gas dedicated for blue hydrogen (i.e. hydrogen production based on natural gas combined with carbon capture and storage) in total supply is projected to increase. With respect to natural gas, the lack of Russian natural gas supply to international markets would not pose a long-term threat to the transition of energy systems.

While the war has put resilience and supply security as top priority for policy making, it also added political arguments to support energy transitions towards reducing import-based fossil fuel dependence. At the same time, inflation and economic uncertainty as well as shortages in material supplies and interrupted/out of balance supply chains increase financing cost for transformation technology and may delay implementation. This is particularly true for those innovations that were supposed to be driven without governmental financial support. Those elements of the transformation that do rely on public support schemes can in turn benefit from the window of opportunity that is created with adding resilience and security of supply as arguments in favour of clean energy transition policies. This is for example true in the chemicals and iron and steelmaking sectors.

Impacts on the global economy and on global greenhouse gas emissions

On the macro-economic scale, the war has introduced an economic crisis in the Russian Federation and Ukraine as well as globally. In OECD projections almost all countries show slower growth than foreseen in projections before the war. For OECD countries, the projection for 2023 is 2 percentage points lower. In terms of greenhouse gas emissions, the current crisis has different effects that partly level each other out. On the one hand, there will be an emissions increase because natural gas will be replaced with other, more emission-intensive fossil fuels. On the other hand, the high prices for energy partly lead to direct and indirect reduction in demand for natural gas (e.g. due to lower levels of gas-consuming industrial activities like ammonia production and higher imports or due to less use of fertilisers, one of the main ammonia-derived products). Energy savings and renewable energy programs as a reaction to reduced natural gas and crude oil supply will also lower emissions. As discussed above, fuel prices are projected to stay high for the next couple of years, which gives a price signal for spurring investment in climate change mitigation technologies and induce behaviour change. A first quantification of the different, partly countervailing effects on the global scale might be available with the upcoming edition of the World Energy Outlook later in October 2022.

Additional actions under the RePowerEU plan

For the EU, the REPowerEU Plan aims to incorporate the various effects on global energy markets, supply chains and induced consumer behaviours. The actions in the REPowerEU Plan cover energy savings, diversification of energy supplies, and accelerated roll-out of renewable energy to replace fossil fuels in all sectors. They cover a dedicated EU Solar Strategy to double solar photovoltaic capacity by 2025 and install 600 GW by 2030, and a Biomethane Action Plan aiming at producing 35 billion cubic metres by 2030.

The modelling accompanying the plan calculates a reduction of 67 percent in gross gas-fired electricity generation compared to the previous Fit-for-55 plan, and around 8 GW less installed gas-fired capacity for the EU in 2030. At the same time, coal-fired electricity supply increases by 105 TWh in 2030. Generation from nuclear also increased by 45 TWh due to maintenance of capacities in Belgium and France. Final energy consumption is assumed to be 4.6 percent lower than in the previous proposal due to higher prices, dedicated policies and consumer awareness. Additional investments in renewable electricity supply capacities and lower energy demand increase the total share of renewable energy in 2030 to 45 percent (compared to 40 percent in the Fit-for-55 proposals). In the residential and services sectors, natural gas use decreases substantially, mainly via electrification, heat pumps and bio-methane transported in the existing gas network. Fossil fuel imports from the Russian Federation are also reduced through significant use of hydrogen in hard-to-abate transport sectors. All together these measures are projected to increase the EU’s emission reduction compared to 1990 levels to 57-58 percent with the REPowerEU Plan.

Impacts on the international climate negotiations

The Russian Federation’s war on Ukraine also complicates diplomatic relationships and events at international level, including the Conference of the Parties (COP) under the United Nations Framework Convention on Climate Change in November 2022. In particular, it can be expected that the war will be addressed in the opening plenary of the COP. This has already been the case in the opening plenary of the Subsidiary Bodies meeting in Bonn in June 2022, when the EU, the Umbrella Group and the Environmental Integrity Group condemned the war and voiced their support for Ukraine. When the Russian Federation took the floor to justify its invasion of Ukraine, delegates of many Parties left the plenary. However, the technical negotiations at the Subsidiary Bodies meeting in June 2022 were not affected, and delegates focused on the specific topics in their interventions without addressing the war.

Role of the Umbrella Group

In the international climate negotiations, most large developed countries outside the EU are members of the Umbrella Group. The Russian Federation, Belarus and Ukraine have been members of the Umbrella Group for many years. In March 2022, an Australian official announced that members of the Umbrella Group were no longer coordinating with Russia and Belarus. However, this has limited practical impact on the negotiations because traditionally the Umbrella Group has coordinated less than other groups. In general, there is no coordinated Umbrella Group position and several members of the group speak for their country rather than for the whole group.

Beyond the climate negotiations, the Russian Federation’s war on Ukraine contributes to a fragmentation of the international community. While many countries express their strong support for Ukraine, some countries, including most notably China, ties to the Russian Federation. Such a fragmentation can make it more difficult to achieve broad support for international initiatives and to organise a coordinated response to threats posed by climate change.

Dr Roman Mendelevitch is an expert in energy system and electricity market modelling at the Oeko-Institut’s Berlin office. He develops scenarios of the future energy supply and designs market-based instruments of climate policy. Hauke Hermann is a Senior Researcher in the Energy and Climate Division. Lorenz Moosmann is an expert for greenhouse gas emissions and reporting at the division ‘Energy & Climate’ at the Berlin office. He participated in the international climate negotiations on transparency as a member of the German delegation.